.svg)

The complex world of insurance fronting represents a significant but often misunderstood aspect of the industry's operational framework. For agency owners navigating this landscape, understanding the nuances of fronting arrangements can unlock strategic advantages while helping avoid potential pitfalls. As insurance technology evolves, companies like Sonant AI are transforming how agencies manage communication aspects of these complex relationships, but the fundamental structures of fronting arrangements remain crucial knowledge for industry professionals.

Understanding the Foundations of Insurance Fronting

Insurance fronting is a specialized arrangement where one insurer (the fronting carrier) issues policies on behalf of another entity that bears most of the financial risk. This practice has evolved into a sophisticated risk management strategy that serves multiple purposes in today's insurance ecosystem.

What Exactly is Insurance Fronting?

At its core, fronting involves a licensed insurance company issuing policies without the intention of retaining most of the risk. What Is Fronting in Insurance and How Does It Work? defines fronting as "the use of a licensed, admitted insurer to issue an insurance policy on behalf of a self-insured organization or captive insurer without the intention of transferring any risk." The fronting carrier typically cedes most or all of the risk back to the originating entity through reinsurance agreements.

Think of it as a form of financial intermediation where the fronting insurer essentially "rents" its license and paper to another entity. The fronting carrier issues the policy documents, handles regulatory filings, and may manage claims processing, while the financial responsibility for claims payments ultimately rests with the reinsurer or risk-bearing entity.

The Legal Framework Behind Fronting

Fronting operates within a complex regulatory environment that varies by jurisdiction. Insurance regulations typically require carriers to be licensed in states where they issue policies, creating barriers to market entry. Fronting arrangements emerged as a practical solution to these regulatory challenges.

The legal basis for fronting varies significantly across jurisdictions but generally adheres to state or national regulations governing insurance operations. Regulatory bodies scrutinize these arrangements to prevent misuse, such as circumventing capital requirements or sidestepping consumer protections. Many jurisdictions require fronting insurers to retain a portion of the risk-typically around 10%-to ensure proper underwriting standards are maintained.

Insurance commissioners across states maintain varying levels of oversight on fronting arrangements. Some states have implemented specific regulations addressing these structures, while others rely on broader regulatory frameworks governing reinsurance and risk transfer.

Navigating Fronting Structures and Relationships

The mechanics of fronting arrangements involve multiple parties and complex contractual relationships. Understanding these structures is essential for agency owners who may be involved in placing business through fronting carriers.

Key Players in Fronting Arrangements

A typical fronting arrangement involves several key participants:

- Fronting Carrier: The licensed insurer that issues the policy and appears as the insurance provider to policyholders and regulators

- Risk-Bearing Entity: The organization assuming the financial responsibility, often a captive insurer, self-insured group, or unlicensed carrier

- Intermediaries: Brokers, managing general agents, and other entities that may facilitate the arrangement

- Regulators: State insurance departments that oversee the arrangement to ensure compliance and consumer protection

Each participant has distinct responsibilities and interests in the arrangement. The fronting carrier focuses on compliance, service delivery, and fee generation, while the risk-bearing entity seeks market access and regulatory compliance without the full burden of licensing requirements.

Contractual Frameworks in Fronting

Fronting arrangements are structured through legally binding contracts that define the relationship between the fronting insurer and the entity assuming financial risk. These contracts outline coverage parameters, premium allocation, claims handling procedures, and financial responsibilities.

According to What Is a Fronting Arrangement and Why Do Captive Insurers Use Them? , fronting agreements typically include:

- Reinsurance agreements specifying risk transfer mechanisms

- Claims handling protocols and authority limits

- Premium payment and funds flow procedures

- Collateral requirements to secure the fronting carrier's position

- Reporting requirements and information sharing protocols

- Termination provisions and run-off procedures

The cost structure of these arrangements typically involves the fronting carrier charging a percentage of gross written premiums—generally between 6% and 10%, depending on the scope of services provided and prevailing market conditions. This fee compensates the fronting carrier for assuming credit risk, providing services, and deploying its licensing and capital.

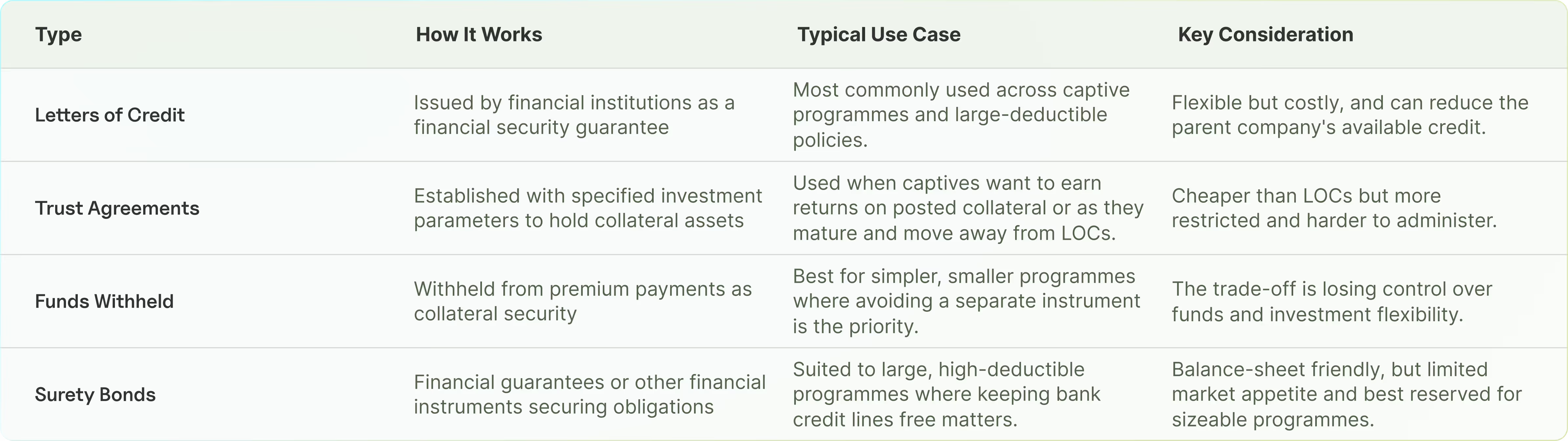

Collateral Requirements in Fronting

A critical aspect of fronting arrangements is the collateral requirement. Fronting carriers typically require the risk-bearing entity to provide financial security to guarantee performance of obligations. This protects the fronting carrier from potential default by the reinsurer.

Common collateral forms include:

- Letters of credit from financial institutions

- Trust agreements with specified investment parameters

- Funds withheld from premium payments

- Surety bonds or other financial guarantees

The collateral amount is typically calculated based on projected claim liabilities and may be adjusted periodically based on actual loss experience and reserve developments. Agency owners should understand these collateral requirements when advising clients on fronting arrangements, as they represent significant financial commitments.

Strategic Benefits and Risk Management in Fronting

For insurance agencies and their clients, fronting arrangements offer several strategic advantages while introducing distinct risk considerations that require careful management.

Why Organizations Use Fronting Arrangements

Organizations employ fronting for various strategic purposes:

- Regulatory Compliance: Fronting allows entities to comply with financial responsibility laws that require coverage from admitted insurers. This is particularly relevant for auto liability, workers' compensation, and other mandated coverages.

- Market Access: Captives and self-insured groups can access markets where they lack licensing through fronting carriers.

- Service Access: Fronting arrangements often include access to the fronting carrier's claims handling infrastructure, loss control services, and other operational capabilities.

- Financial Flexibility: These structures can provide potential tax advantages and cash flow benefits compared to traditional insurance purchases.

The primary purpose of fronting is compliance with insurance regulations. However, an important secondary purpose is accessing services such as claims handling and risk control, as well as excess risk transfer capacity, from the fronting insurer in a cost-effective manner. For agencies utilizing AI in insurance automation , these arrangements can be particularly valuable when integrated with modern technology solutions.

Risk Considerations in Fronting Relationships

While fronting offers significant benefits, it also introduces unique risks that require careful management:

- Credit Risk: The fronting carrier faces the risk that the reinsurer may default on obligations

- Operational Risk: Misalignment in claims handling philosophies or service expectations can create friction

- Regulatory Risk: Changes in regulatory requirements or interpretations may impact the viability of fronting structures

- Reputational Risk: The fronting carrier's brand is associated with policies it doesn't fully control

Disputes in fronting arrangements often arise when claims are denied, delayed, or contested based on policy interpretations. The fronting insurer issues the policy and makes initial coverage determinations, but the reinsurer bears the financial burden. This dynamic can create tension, especially when significant claims arise.

Agencies should help clients understand these risk dimensions and establish clear protocols for addressing potential conflicts. Implementing an AI receptionist for insurance can help manage communication challenges that often arise in these complex arrangements.

Captive Insurers and Fronting

Captive insurance companies frequently utilize fronting arrangements to overcome regulatory barriers and access specialized services. A captive insurer, owned by the insureds themselves, primarily covers the risks of its owners and operates outside traditional insurance markets.

For captives, fronting solves several critical challenges:

- Enabling compliance with admitted insurance requirements

- Providing access to states where the captive lacks licensing

- Facilitating the issuance of certificates of insurance and policy documents

- Accessing claims administration infrastructure

The relationship between captives and fronting carriers represents one of the most common and established fronting models in the industry. Agency owners working with captive structures should thoroughly understand fronting carrier selection criteria and relationship management best practices.

Selecting the Right Fronting Partner

For insurance agencies advising clients on fronting arrangements, helping select the appropriate fronting carrier is a critical value-added service. This decision has long-term implications for program success.

Evaluation Criteria for Fronting Carriers

When evaluating potential fronting partners, agencies should consider several key factors:

- Financial Strength: The fronting carrier's financial ratings and stability are paramount

- Licensing Footprint: Ensure the carrier is licensed in all jurisdictions where coverage is needed

- Industry Experience: Specialized knowledge in the client's industry sector is valuable

- Service Capabilities: Assess claims handling, loss control, and administrative capabilities

- Technology Infrastructure: Modern systems facilitate smoother operations and reporting

- Relationship Approach: The carrier's philosophy on partnership and collaboration matters

Agencies should conduct thorough due diligence on potential fronting partners, including reference checks with existing clients. For evaluating the financial impact of different arrangements, tools like the Live Transfer ROI Calculator can provide valuable insights into cost-benefit analyses.

Negotiating Fronting Agreements

Once a fronting carrier is selected, negotiating favorable terms becomes the next challenge. Key negotiation points typically include:

- Fronting Fees: The percentage charged on gross written premium

- Collateral Requirements: The amount, form, and adjustment mechanisms

- Claims Authority: Decision-making parameters and escalation protocols

- Service Level Agreements: Performance metrics and accountability mechanisms

- Information Access: Reporting requirements and data sharing protocols

- Termination Provisions: Exit conditions and run-off management

Agencies can add significant value by guiding clients through these negotiations, leveraging industry knowledge to secure favorable terms. Understanding market standards and having benchmark data strengthens negotiating positions.

Technology and the Future of Fronting Management

The landscape of insurance fronting is evolving rapidly as technology transforms how these arrangements are structured, implemented, and managed. For agency owners, staying ahead of these trends is essential for providing strategic advice to clients.

Digital Transformation in Fronting Operations

Technology is revolutionizing fronting operations across several dimensions:

- Automated Compliance Monitoring: Systems that track regulatory requirements across jurisdictions

- Real-time Data Exchange: APIs and integration platforms facilitating seamless information flow

- Blockchain Applications: Distributed ledger technology creating transparent, immutable records of transactions

- Predictive Analytics: Advanced modeling to optimize collateral requirements and pricing

- Robotic Process Automation: Streamlining administrative tasks and reducing operational friction

These technological advances are reducing administrative burdens, improving transparency, and enabling more sophisticated risk analysis. Agencies that optimize your workflow with integrations can better support clients in managing these increasingly digital fronting relationships.

Communication Challenges in Fronting Relationships

One persistent challenge in fronting arrangements is managing communication across multiple stakeholders. These relationships involve numerous parties—the insured, the agency, the fronting carrier, the risk-bearing entity, and often multiple service providers.

Traditional communication methods can lead to delays, misunderstandings, and operational inefficiencies. Modern agencies are addressing these challenges through:

- Centralized communication platforms

- Automated notification systems

- Standardized reporting templates

- Regular stakeholder coordination meetings

For agencies looking to improve efficiency and customer satisfaction, exploring AI-powered live transfer leads could be a game-changer in managing these complex relationships. These solutions help ensure that communication flows smoothly across all parties involved in fronting arrangements.

Emerging Trends in Fronting Arrangements

Several emerging trends are reshaping the fronting landscape:

- Specialized Fronting Carriers: The rise of carriers focused exclusively on fronting services

- Program Business Expansion: Growing utilization of fronting in program and MGA structures

- InsurTech Partnerships: Collaboration between traditional fronting carriers and technology platforms

- Alternative Risk Transfer: Integration of fronting with parametric insurance and other innovative structures

- Enhanced Analytics: Data-driven approaches to optimizing fronting structures

These trends point toward a more flexible, efficient fronting ecosystem that offers expanded options for agencies and their clients. Staying informed about these developments enables agencies to provide forward-looking advice on fronting strategies.

For those looking to enhance their agency's efficiency in managing these complex relationships, exploring the role of AI in agency operations can provide valuable insights into emerging best practices.

Regulatory Oversight and Compliance Considerations

Regulatory compliance remains a central consideration in fronting arrangements, with oversight frameworks continuing to evolve in response to market developments.

Current Regulatory Landscape

Regulatory bodies review financial statements, risk retention levels, and reserve adequacy to confirm the insurer can cover claims if the reinsurer defaults. Solvency requirements, such as risk-based capital thresholds, prevent insurers from overextending themselves in fronting arrangements.

Key regulatory focus areas include:

- Minimum risk retention requirements for fronting carriers

- Collateral adequacy standards and monitoring

- Disclosure requirements to policyholders

- Reinsurance agreement terms and conditions

- Financial reporting and transparency measures

The National Association of Insurance Commissioners (NAIC) and individual state insurance departments continue to refine their approaches to fronting oversight, with increasing emphasis on consumer protection and market stability.

Compliance Best Practices

Agencies advising clients on fronting arrangements should promote robust compliance practices:

- Conducting thorough due diligence on all parties in the arrangement

- Maintaining comprehensive documentation of program structures

- Implementing regular compliance reviews and audits

- Establishing clear protocols for regulatory interactions

- Monitoring regulatory developments across relevant jurisdictions

To improve efficiency in handling insurance documents related to fronting arrangements, consider utilizing an AI-powered policy comparison tool to automate the review process and ensure consistent compliance.

Practical Guidance for Agency Owners

For agency owners navigating the complexities of fronting arrangements, practical guidance can help maximize value while minimizing risks.

When to Consider Fronting Arrangements

Fronting arrangements are particularly valuable in specific scenarios:

- When clients require admitted paper for regulatory or contractual reasons

- For captive insurance programs seeking market access

- When specialized risk management capabilities are needed

- For multi-state operations requiring uniform coverage

- When traditional markets are unavailable or uncompetitive

Agencies should help clients evaluate whether fronting aligns with their risk management objectives and operational requirements. This assessment should consider both immediate needs and long-term strategic goals.

Managing Client Expectations

Setting appropriate client expectations is crucial for successful fronting relationships:

- Clearly explain the roles and responsibilities of all parties

- Set realistic timeframes for implementation and service delivery

- Outline potential challenges and mitigation strategies

- Establish transparent communication protocols

- Define success metrics and performance indicators

Agencies should position themselves as strategic advisors throughout the fronting relationship lifecycle, providing ongoing guidance as programs evolve. To streamline operations and improve customer interactions, many companies are turning to AI solutions for insurance offered by Sonant AI.

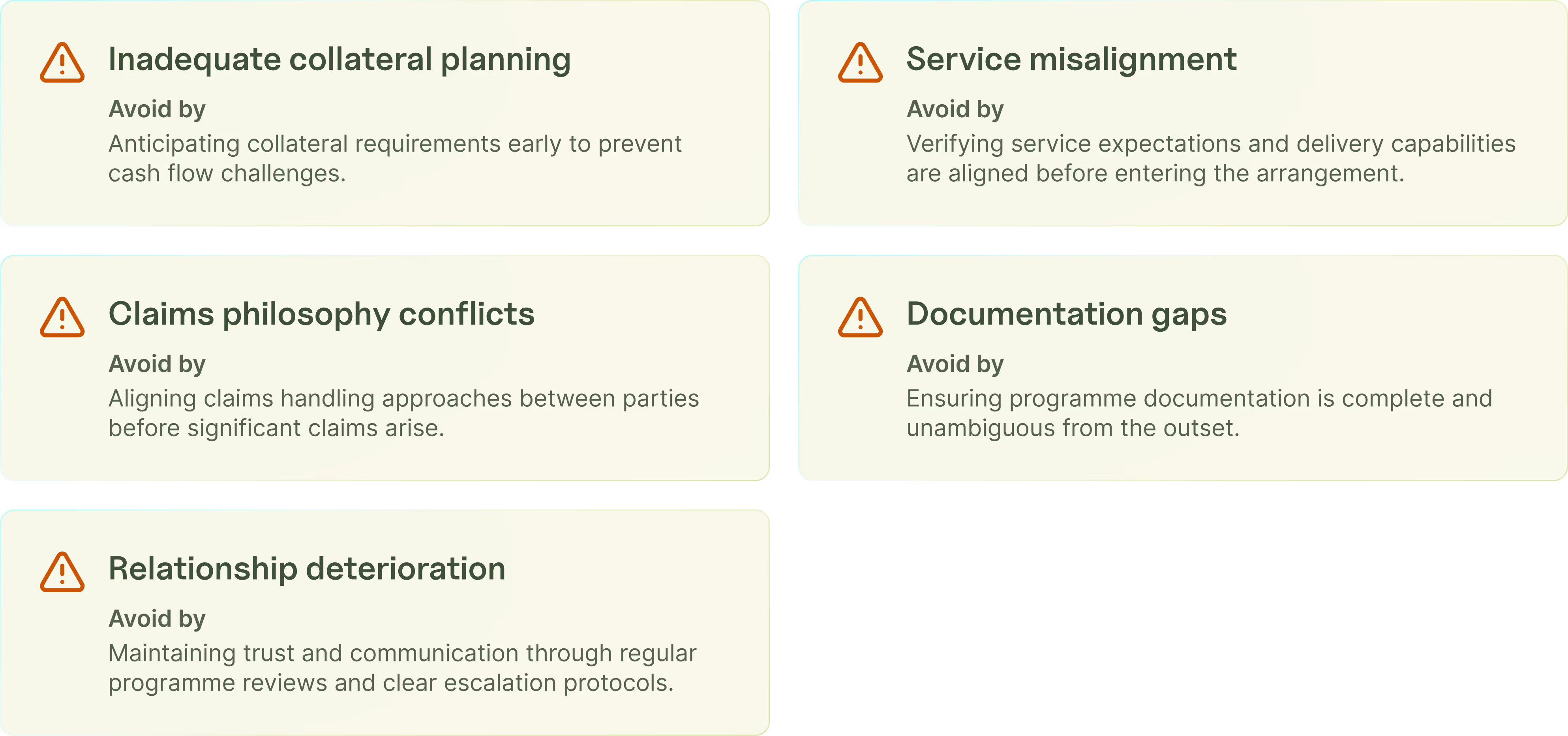

Common Pitfalls and How to Avoid Them

Several common pitfalls can undermine fronting arrangements:

- Inadequate Collateral Planning: Failing to anticipate collateral requirements can create cash flow challenges

- Service Misalignment: Disconnects between service expectations and delivery capabilities

- Claims Philosophy Conflicts: Differences in claims handling approaches between parties

- Documentation Gaps: Incomplete or ambiguous program documentation

- Relationship Deterioration: Erosion of trust and communication between parties

Proactive management of these risk factors is essential for program success. Regular program reviews, clear escalation protocols, and relationship maintenance strategies help prevent these issues from undermining fronting arrangements.

To explore more about how AI is transforming the sector, check out this article on AI in insurance industry .

Conclusion: Mastering Fronting for Agency Success

Insurance fronting represents a sophisticated risk management strategy that offers significant benefits when properly structured and managed. For agency owners, developing expertise in fronting arrangements creates opportunities to deliver enhanced value to clients while differentiating service offerings in competitive markets.

The key to success lies in understanding the fundamental mechanics of fronting, carefully selecting and managing fronting relationships, staying ahead of regulatory developments, and leveraging technology to streamline operations. As with many aspects of insurance, the details matter-thorough documentation, clear communication, and proactive problem-solving are essential.

As fronting continues to evolve, agencies that develop specialized expertise in these arrangements will be well-positioned to guide clients through increasingly complex risk management challenges. To explore the future of customer service in this evolving landscape, consider how AI in insurance automation is transforming interactions and policy management.

By mastering the intricacies of insurance fronting, agency owners can unlock new strategic opportunities while helping clients navigate the complex regulatory and operational landscape of modern risk management.

The AI Receptionist for Insurance

FOLLOW SONANT ON

.svg)

.svg)