.svg)

Starting an Insurance Agency: A Financially Transparent Blueprint

Starting an insurance agency is not a passive-income shortcut. It demands 12 to 24 months of sustained effort before most owners see consistent profitability - and that timeline assumes you make smart decisions from day one. If someone told you otherwise, they were selling something.

The insurance industry offers two primary agency models: captive and independent. Captive agents represent a single carrier exclusively, while independent agencies represent multiple insurance carriers. Each model carries radically different economics, support structures, and long-term equity implications. Choosing the wrong one for your situation can cost you years.

This guide delivers hard numbers, not motivational clichés. Wolters Kluwer reports over 75,000 federal, state, and local jurisdictions carry compliance requirements that new agency owners must navigate. That statistic alone underscores the complexity of doing this right. Whether you want to start an insurance agency from scratch or transition an existing book, you need a plan grounded in financial reality.

Here is what we cover: the self-assessment, the captive-vs-independent decision, licensing, Errors & Omissions (E&O) insurance, technology infrastructure, first-year cash flow, carrier appointments, hiring, and a 90-day launch plan. Whether you're evaluating your first hire or your first AI tool for your agency, the economics have to work first.

Is Agency Ownership Right for You? A Realistic Self-Assessment

Five questions you must answer honestly

Before you spend a dollar on licensing or letterhead, sit with these questions:

- Do you have 12 to 18 months of personal living expenses saved? Your agency will not pay your mortgage in month two. Period.

- Are you comfortable earning $0 in months one through three? Most new agencies generate little to no commission income during the initial quarter.

- Can you sell and service simultaneously? You will wear every hat - producer, customer service rep, compliance officer, and janitor - until revenue justifies your first hire.

- Do you understand insurance products deeply enough to advise, not just transact? Clients trust advisors who know coverage gaps, not order-takers who read from a script.

- Are you willing to handle compliance, HR, and technology on day one? Managing agency management software and regulatory filings is your responsibility from the start.

The consequences of half-measures

Insurance Business Magazine warns that selling insurance without the necessary licenses can result in a felony charge, substantial fines, blocked commissions, and license revocation. Half-measures are not an option in this industry.

The timeline alone should temper unrealistic expectations. The Insurors of Tennessee notes that opening a new insurance agency takes at least six months to arrange financing and at least 30 days to obtain E&O insurance before you can even pursue carrier appointments. This is not a business you launch over a weekend.

Know which type of founder you are

Your background shapes your advantages and blind spots:

- Experienced producers going independent: You bring a book of business and carrier relationships. Your challenge is building the operational backbone you previously took for granted

- Career changers with capital: You offer fresh perspective and funding. Your disadvantage is zero pipeline and no industry network

- Entrepreneurs entering insurance: You bring business acumen and systems thinking. Your learning curve centers on licensing, lead generation, and product knowledge

If your self-assessment checks out, the rest of this guide shows exactly how to build the financial model.

Captive vs Independent: The Economics Deep-Dive

Commission economics compared

The single biggest financial decision in how to start an insurance agency is choosing between captive and independent models. This choice affects every dollar you earn for the life of your business.

Captive agents typically earn 8% to 12% new-business commissions on property and casualty lines, with renewal commissions ranging from 2% to 4%. The carrier absorbs marketing costs, provides leads, and offers a recognizable brand. Independent agents earn 12% to 20% new-business commissions and 10% to 15% on renewals - significantly higher per policy.

But higher commissions come with higher costs. Independent agents pay for their own technology, marketing, office space, and E&O insurance. Captive agents often receive subsidized or free access to these resources.

Support and infrastructure trade-offs

Captive carriers like State Farm, Allstate, and Farmers run structured onboarding programs. They provide training curricula, mentorship, marketing materials, and sometimes even office subsidies during the first year. You trade earning potential for guardrails.

Independent agencies must build everything from scratch. You select your own agency management system (AMS), design your workflows, source your leads, and negotiate every carrier appointment. The upside? You own the client relationships. The downside? Every operational failure is yours to fix. Building strong customer service strategies from the start becomes critical for retention.

Equity value and exit implications

This is where the models diverge most dramatically. Captive agents generally do not own their book of business - the carrier does. If you leave a captive arrangement, you may forfeit the client relationships you built over years. Some captive programs offer partial ownership or buyout provisions, but the terms heavily favor the carrier.

Independent agents own their book outright. A well-run independent agency with $500,000 in annual revenue and strong retention rates might sell for 1.5x to 2.5x revenue. That equity represents real, transferable wealth. You can use our free agency valuation calculator to estimate what your book could be worth at various growth milestones.

The captive path: What the programs actually look like

State Farm's Agent Aspirant program typically requires candidates to work as team members before receiving their own agency. Allstate's program offers a monthly subsidy during the build phase but requires meeting production minimums. Farmers provides a protected territory and a structured development timeline.

Each program has minimum net worth requirements, location restrictions, and performance benchmarks that can terminate your agreement if unmet. Read the fine print.

The independent path: Carrier appointments and cluster options

fronting arrangements explained

Going independent means securing appointments with multiple carriers - and carriers are selective. Most require minimum premium volume commitments, proven production history, and E&O coverage before they will consider your application. New agencies with no track record often start with two to four carriers and build from there.

Cluster groups and aggregators offer a shortcut. Organizations like SIAA, Smart Choice, and Renaissance Alliance allow new agencies to access carrier appointments under the group's umbrella. You sacrifice a portion of your commission (typically 10% to 20% of the override) in exchange for immediate market access. For many insurance agency startups, this trade-off accelerates the path to viability.

Legal and Licensing Requirements by State

Individual producer licensing

Every state requires individual insurance producers to pass a state-administered licensing exam. Licensing requirements vary by state, but typically involve pre-licensing education, passing exams, and meeting specific eligibility criteria. The two most common license types are a Property and Casualty (P&C) license and a Life, Health and Accident license.

Some states have d the process. Tennessee, for example, no longer requires a pre-licensing class to sit for the licensing exam. Other states mandate 40 to 60 hours of pre-licensing education before you can test.

The Producer Licensing Model Act from the National Association of Insurance Commissioners (NAIC) lists eight major lines of authority, each requiring separate insurance licenses. You need the right license for every product you sell - no exceptions.

Agency and business entity licensing

Beyond individual licensing, most states require a separate agency license tied to your business entity. You will need a designated responsible licensed producer (DRLP) - a licensed professional responsible for ensuring your agency complies with state laws and regulations.

Many states prohibit using terms like "insurance," "assurance," or "underwriter" in a business name unless the entity holds proper licensure. Check your state's naming restrictions before filing your LLC or corporation paperwork.

Continuing education and renewal

Insurance licenses must be renewed every one to three years, depending on the state. Most states require continuing education (CE) courses for renewal. Falling behind on CE can trigger license suspension, which immediately halts your ability to earn commissions and serve clients.

State insurance divisions like the Tennessee Insurance Division regulate and license both individuals and corporations, assess fraud, and enforce compliance. In 2024 alone, Tennessee's mediation efforts returned $17.54 million to consumers - a reminder that regulators actively protect the marketplace.

Data protection compliance

Insurance agencies must safeguard client information under data protection laws such as the Gramm-Leach-Bliley Act (GLBA). You will need privacy notices, data handling procedures, and secure systems from day one. Agencies investing in conversational AI solutions should verify that any technology partner meets these compliance standards.

E&O Insurance: Requirements and Costs

Why E&O comes before everything else

Errors & Omissions insurance protects your agency against claims of negligence, misrepresentation, or failure to provide adequate coverage advice. Nearly every carrier requires proof of E&O coverage before granting an appointment. No E&O, no appointments. No appointments, no revenue.

E&O policies for new agencies typically cost $2,500 to $5,000 annually for $1 million in coverage. Premiums vary based on your lines of authority, state, premium volume, and claims history. Expect to pay at the higher end if you write commercial lines.

Selecting the right E&O policy

Look for policies that cover:

- Claims arising from failure to procure coverage

- Errors in policy binding or documentation

- Allegations of misrepresentation

- Defense costs in addition to (not included within) policy limits

- Prior acts coverage if you are transitioning from another agency

Budget for E&O as a fixed cost. It does not go away, and it should not be the line item you cut when cash gets tight. Agencies that invest in claims automation often reduce documentation errors that trigger E&O claims in the first place.

Technology Infrastructure: Your Minimum Viable Stack

Essential systems for launch

You do not need enterprise-grade technology on day one. But you do need systems that scale. Here is the minimum viable tech stack for a new insurance agency startup:

Where AI fits from day one

New agencies face a paradox: you need to answer every call to build your book, but you also need to be out selling to generate those calls. This is where Sonant AI and similar AI virtual receptionists solve a real operational problem.

An AI receptionist handles inbound calls 24/7, qualifies leads, captures client information, and routes opportunities to you - all without requiring a salaried employee. For a solo agency owner who splits time between prospecting and servicing, this technology can mean the difference between catching a $5,000 annual premium client and sending them to voicemail.

Agencies concerned about client reception should read how one agency handled AI adoption successfully. The key is configuring the tool to match your agency's voice and workflow, not deploying generic automation. Consider AI voice agents as your first "employee" - one that works every shift without overtime.

Integrations matter more than features

When evaluating any technology, ask one question first: does it integrate with my AMS? Disconnected systems create data silos, duplicate work, and compliance gaps. Your CRM should feed your AMS. Your phone system should log to your CRM. Your quoting tools should pull from your AMS. Build a connected stack from the start, and you will avoid painful migrations later. Implementing AI in your agency follows the same principle - integration first, features second.

First-Year Financial Model: The Numbers That Matter

insurance agency startup costs breakdown

Startup cost scenarios

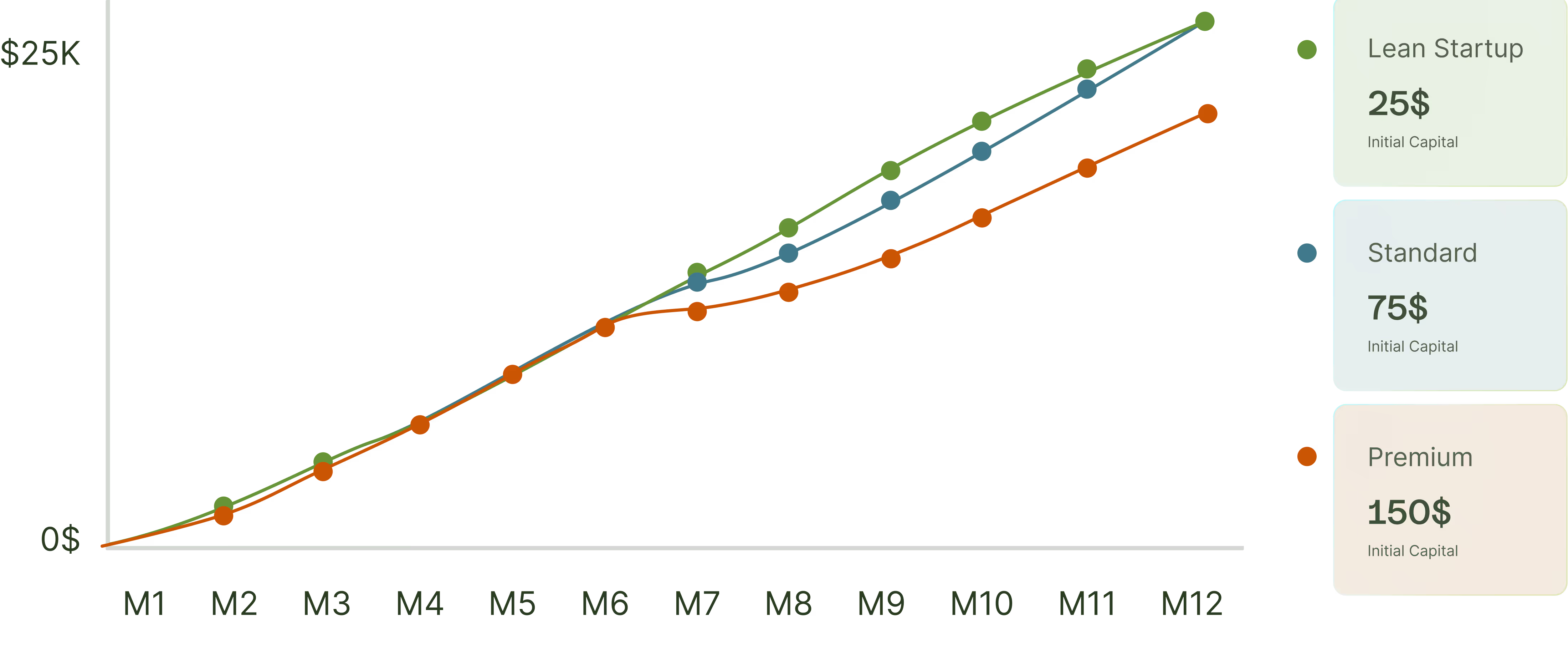

What does it actually cost to open an insurance agency? The answer depends on your model, location, and ambition. Here are three realistic scenarios:

Realistic revenue ramp: Months 1 through 12

New independent agencies following a disciplined prospecting schedule typically write $5,000 to $15,000 in monthly premium by month six. At a 15% average commission rate, that translates to $750 to $2,250 in monthly commission income. Not enough to cover expenses yet.

By month nine to 12, agencies with consistent prospecting habits reach $25,000 to $40,000 in monthly written premium. Commission income climbs to $3,750 to $6,000 monthly. Add renewal commissions from early policies, and you begin approaching break-even.

These numbers assume a solo producer writing personal lines and small commercial. Agencies focused on auto insurance live transfers and other lead sources can accelerate the ramp, but paid leads add to your cost basis.

Cash burn and runway planning

Most new agencies burn $3,000 to $6,000 per month in fixed costs (E&O, technology, phone, office or coworking space, marketing). Variable costs like lead purchases and travel add another $1,000 to $3,000 monthly during active prospecting.

At a $5,000 monthly burn rate, a $30,000 reserve gives you six months of runway. That is tight. A $75,000 reserve provides 15 months - enough to reach the break-even zone with margin for error. We recommend the latter for anyone serious about building a sustainable agency.

Break-even timeline scenarios

Three realistic break-even timelines based on production pace:

- Aggressive producer (150+ quotes/month): Break-even at months eight to 10

- Moderate producer (80-120 quotes/month): Break-even at months 12 to 16

- Conservative producer (40-70 quotes/month): Break-even at months 18 to 24

Investing in renewal automation early helps protect the revenue you generate. Every policy that lapses due to a missed follow-up is money you already earned walking out the door.

Getting Appointed: Direct vs Cluster/Aggregator

Direct Bold Penguin alternativecarrier appointments

Securing direct appointments with carriers requires demonstrating production capability. Most carriers want to see:

- Active state licenses in your lines of authority

- Current E&O coverage meeting their minimum limits

- A business plan with premium volume projections

- A physical or virtual office address

- Clean background check and credit history

Regional and mutual carriers tend to be more receptive to new agencies than national carriers. Start with three to four carrier appointments that cover personal auto, homeowners, and a basic commercial package. You can add specialty markets as your book grows.

Cluster groups and aggregators

If you cannot secure direct appointments - or want broader market access immediately - cluster groups provide a viable alternative. Under a cluster arrangement, you write business through the group's carrier contracts and share a portion of the commission override.

The economics work like this: if a carrier pays 15% commission with a 3% override, the cluster keeps the override (or splits it with you) while you retain the base 15%. Some clusters charge flat monthly fees instead. Compare total cost carefully before signing.

Cluster groups also provide access to multilingual support resources and shared technology platforms that would cost individual agencies significantly more to deploy independently.

First Hires: When and Who

The solo phase: Months 1 through 6

Resist the urge to hire immediately. Your first six months should be about learning every function of the business firsthand. You cannot manage what you have never done. Answer the phones. Process the endorsements. Handle the claims calls. This knowledge becomes invaluable when you eventually delegate.

During this phase, technology substitutes for headcount. An AI-powered 24/7 support system handles after-hours calls. A good AMS automates renewal reminders. An online rater speeds quoting. These tools keep your cost basis low while you build revenue.

Your first hire: The customer service representative

When your service workload consumes more than 50% of your day - typically around months six through nine - it is time to hire. Your first employee should be a licensed customer service representative (CSR), not a second producer.

Why? Because service work is what prevents you from selling. A CSR handles endorsements, certificates of insurance, billing questions, and basic claims intake. This frees you to quote, close, and prospect - the activities that actually grow revenue. Consider hiring a virtual assistant if a full-time salary is not yet feasible.

Scaling with technology before headcount

Before hiring a second or third employee, exhaust your technology options. AI-driven efficiency tools can handle tasks that previously required dedicated staff:

- AI call assistants qualify and route inbound calls without human intervention

- Automated claims workflows reduce manual processing time by hours per week

- Claims automation platforms handle first notice of loss intake

- AI-powered retention tools identify at-risk clients before they shop

Agencies that recently cut missed calls by 50% with AI provide a useful case study. One Canadian brokerage deployed Sonant AI and dramatically improved its call capture rate without adding staff. For a new agency watching every dollar, that approach makes financial sense.

Your First 90 Days: Action Plan

Days 1 through 30: Legal and licensing foundation

- Form your business entity (LLC recommended for liability protection)

- Register your business name - confirm compliance with state naming restrictions

- Complete pre-licensing education (if required by your state)

- Pass your state licensing exams for P&C and/or Life and Health

- Apply for your resident producer license

- Apply for your agency license and designate your DRLP

- Secure your E&O insurance policy

- Open a business bank account and establish bookkeeping

Days 31 through 60: Technology and carrier setup

- Select and configure your AMS (Applied Epic, HawkSoft, or QQCatalyst for new agencies)

- Set up your CRM for prospect tracking

- Deploy your phone system with an AI receptionist for remote service capability

- Submit carrier appointment applications (start with three to four carriers)

- Join a cluster group if direct appointments are not yet available

- Build your website and Google Business Profile

- Begin SEO groundwork for long-term organic lead generation

Days 61 through 90: Revenue generation begins

- Launch outbound prospecting - 20 to 30 calls per day minimum

- Activate paid lead sources (start small, measure cost per bind)

- Write your first policies and celebrate the milestone (seriously)

- Establish a weekly review cadence: quotes issued, policies bound, premium written, close ratio

- Solicit referrals from every new client within 30 days of binding

- Review and adjust your budget against actual cash flow

- Document every process you perform - you will need these SOPs when you hire

The first 90 days set the operational DNA of your agency. Build disciplined habits now and they compound. Skip steps and you will spend months cleaning up avoidable problems.

Building an Agency That Lasts

Starting an insurance agency demands more capital, more patience, and more grit than most business guides admit. The producers who succeed treat this as a two-year project, not a two-month experiment. They plan their finances conservatively, invest in systems early, and resist the temptation to scale before the economics support it.

The independent model offers superior long-term economics for those willing to endure the harder first year. Captive programs provide structure and support for those who need guardrails. Neither path is wrong - but choosing the wrong path for your situation is expensive.

At Sonant AI, we work with hundreds of agencies across the growth spectrum - from solo producers in their first year to established firms scaling past $5 million in premium. The pattern we see consistently: agencies that invest in smart operational infrastructure early reach profitability faster and retain clients at higher rates than those who try to do everything manually.

The phone is going to ring. When it does, your ability to answer it - professionally, promptly, and with the right information - determines whether that caller becomes a client or calls your competitor. Build the foundation right, and every year gets easier than the last.

The AI Receptionist for Insurance

FOLLOW SONANT ON

.svg)

.svg)