.svg)

Introduction

Claims adjusters now handle 150 to 200 claims simultaneously while coordinating with repair shops, medical providers, and multiple stakeholders - a reality that strains even the most experienced professionals. This operational burden creates a breaking point where quality service becomes nearly impossible to maintain. Meanwhile, $170 billion in global insurance premiums sit at risk by 2027 due to poor claims experiences that erode policyholder trust and loyalty.

The opportunity cost extends beyond customer satisfaction. Traditional manual workflows create delays where claims sit in queues for days or weeks, consuming valuable production time that could be spent building client relationships and closing new business. Yet the transformation is already underway: automation reduces claim processing times by up to 50% while cutting operational costs by 20-30%.

This guide provides the definitive roadmap for insurance agencies ready to reclaim production time and convert every claim into a trust-building opportunity. We'll explore how insurance claims automation transforms routine interruptions into revenue opportunities, enabling your team to focus on what truly matters - protecting relationships while scaling operations. At Sonant AI, we've helped hundreds of agencies implement intelligent systems that turn every incoming claim call into a experience that strengthens rather than strains client bonds.

What is Insurance Claims Automation?

Claims automation represents the use of digital technologies to manage and process insurance claims with minimal human intervention. Rather than relying on paper-based or manual systems, intelligent automation systems the entire workflow from first contact through final settlement. This transformation touches every stage of the claims lifecycle - from First Notice of Loss (FNOL) through investigation, documentation, adjudication, and payment.

Manual systems create predictable bottlenecks. In traditional workflows, a healthcare provider submits a claim for a patient's treatment only to have it sit in a queue for days or weeks awaiting review. Automation eliminates these delays by flagging errors instantly and routing clean claims for immediate processing. The technology stack includes several core components:

- Robotic process automation (RPA) handles repetitive data entry and validation tasks

- Intelligent document processing (IDP) extracts information from forms, photos, and PDFs

- Machine learning algorithms detect patterns, predict outcomes, and identify potential fraud

- Voice AI captures claim details through natural conversation, providing immediate acknowledgment and next steps

Voice AI systems transform how agencies handle incoming claim calls, offering 24/7 availability and consistent service quality. The impact on accuracy proves substantial - automation can reduce processing errors by up to 80% while dramatically accelerating document handling.

Manual Claims Processing Automated Claims Processing 7-10 day average delay Processing in minutes to hours High error rates from data entry 80% reduction in errors Limited availability (business hours) 24/7 claim intake Inconsistent customer experience Standardized, quality service

A global third-party administrator cut claim lifecycle by 50% with $1.3 million in savings by implementing automated document management. The technology doesn't replace human expertise - it amplifies it by handling routine tasks and freeing adjusters to focus on complex, high-value claims that require judgment and relationship skills. Modern claims automation systems integrate ly with existing agency management systems, creating a unified workflow that captures every detail without duplicating effort.

The Business Case: Why Insurance Claims Automation Matters Now

The insurance industry wastes between $17 billion and $32 billion annually on non-core administrative activities, with underwriters spending up to 40% of their time on tasks that generate zero revenue. This operational drag compounds as adjusters struggle to manage unprecedented caseloads - handling 150 to 200 claims simultaneously leaves little bandwidth for the personalized service that differentiates exceptional agencies from average ones.

Escalating operational pressures

Climate change drives claim frequency and severity upward. Annual insured losses from natural disasters now exceed $100 billion, with total global catastrophe costs reaching $151 billion per year. Agencies face mounting pressure to process higher volumes faster while maintaining quality standards. Yet talent shortages create a paradox: 93% of insurance CEOs plan to expand their workforce over the next three years, but 62% express concern about finding qualified candidates.

The math reveals the problem's scale. In a 2022 American Hospital Association survey of nearly 800 hospitals, institutions collectively reported $6.4 billion in delayed or unpaid claims aged at least six months. Furthermore, 70% of denied claims were eventually paid - but only after multiple costly reviews that strain resources and delay care.

The competitive advantage of early adoption

Insurers implementing workflow automation report an average 65% reduction in total operational costs by automating customer onboarding, policy management, and claims workflows. More critically, AI-powered tools led to a 63% increase in customer satisfaction among insurers using intelligent claims assistance, with time-to-settlement down by 35-40% for mid-sized carriers.

McKinsey research indicates that adjusters in 2025 spend most of their time on complex and high-stakes claims, while more than half of claims processing activities are handled by technology. This shift creates a strategic inflection point: agencies that automate routine tasks position their talent for higher-value work that drives growth and deepens client relationships. Those that delay face widening operational gaps as competitors pull ahead.

Financial impact across the value chain

Automation in fraud detection allows insurers to identify fraudulent claims 50% faster, using machine learning to detect patterns and flag potential fraud in real time. This capability reduces payouts on fraudulent claims by up to 40%, protecting premium pools and reducing costs for honest policyholders. The technology pays for itself quickly - U.S. healthcare providers could save up to $16.3 billion annually by automating claims management alone.

The AI in insurance market tells the adoption story in hard numbers. Expected to grow from $8.13 billion in 2024 to $10.82 billion in 2025, projections show the market reaching $141.44 billion by 2034 at a compound annual growth rate of approximately 33%. Over 80% of insurers now consider AI a top-tier strategic priority for growth and differentiation. The question shifts from whether to automate to how quickly agencies can implement systems that protect their market position.

Core Technologies Powering Insurance Claims Automation

FNOL (First Notice of Loss) automation

Four foundational technologies work in concert to transform claims processing from manual drudgery into d intelligence. Each addresses specific workflow bottlenecks while integrating with the others to create comprehensive automation capabilities that reduce errors, accelerate processing, and free human talent for higher-value work.

Robotic process automation (RPA)

RPA software bots execute repetitive, rule-based tasks with perfect consistency. These digital workers log into systems, extract data from forms, validate information against policy terms, and populate fields across multiple platforms - all without human intervention. A typical claims workflow involves 15 to 20 distinct data entry points across agency management systems, carrier portals, and communication platforms. RPA eliminates this redundant work, reducing processing time from hours to minutes.

The technology excels at handling high-volume, standardized claims. Simple auto glass repairs, minor property damage, and routine medical claims follow predictable patterns that RPA handles efficiently. Bots work 24/7 without breaks, sick days, or vacation time, creating operational capacity that scales instantly with demand spikes following major weather events or accidents.

Intelligent document processing (IDP)

IDP extends beyond basic optical character recognition to understand context, extract relevant information from unstructured documents, and classify content intelligently. The system processes photos from accident scenes, medical records, repair estimates, and police reports - transforming visual information into structured data that feeds directly into claims workflows. This capability proves particularly valuable as mobile claim submissions increase. Policyholders snap photos of damage, submit documentation through apps, and expect immediate acknowledgment and status updates.

Machine learning algorithms continuously improve IDP accuracy by learning from corrections and new document types. A system that initially requires human review for 30% of documents might reduce that ratio to 5% within six months as the model learns to handle variations in format, handwriting, and image quality. This learning curve accelerates return on investment while maintaining the accuracy standards critical for regulatory compliance.

Machine learning for decision support

ML algorithms analyze historical claims data to predict outcomes, estimate settlement ranges, and identify anomalies that warrant human review. These models consider hundreds of variables - claim amount, policy type, claimant history, location, adjuster experience, repair shop ratings - to generate recommendations that support consistent decision-making. Pattern recognition capabilities detect fraudulent claims by identifying suspicious combinations of factors that human reviewers might miss when examining cases individually.

The technology also s resource allocation. ML models predict which claims require specialized expertise, which can route to automated settlement, and which present litigation risk requiring early legal review. This intelligent triage ensures that adjusters spend time where their expertise creates the most value - complex cases involving severe injuries, disputed liability, or significant property damage.

Voice AI for natural interaction

Sonant AI in claims management

Voice AI represents the customer-facing layer that makes automation feel personal rather than mechanical. Modern systems handle inbound calls with human-like conversation, capturing FNOL details through natural dialogue that adapts to caller emotion and communication style. Voice-powered systems provide immediate acknowledgment, schedule adjuster appointments, explain next steps, and answer common questions - all while accurately documenting every detail in the agency management system.

The technology supports multiple languages and dialects, ensuring consistent service for diverse policyholder populations. It never puts callers on hold, loses patience, or fails to capture critical information. For agencies, this means zero missed calls, complete documentation, and the ability to offer 24/7 claim reporting without staffing night shifts. Voice AI integrates with the other automation technologies, triggering RPA workflows, initiating IDP document processing, and feeding ML models with structured data that improves predictions over time.

Implementation Roadmap: From Planning to Full Deployment

Successful automation requires methodical planning and phased execution. Agencies that rush implementation without proper groundwork encounter integration failures, staff resistance, and underwhelming results. Those that follow a structured approach see rapid value realization and smooth adoption across teams.

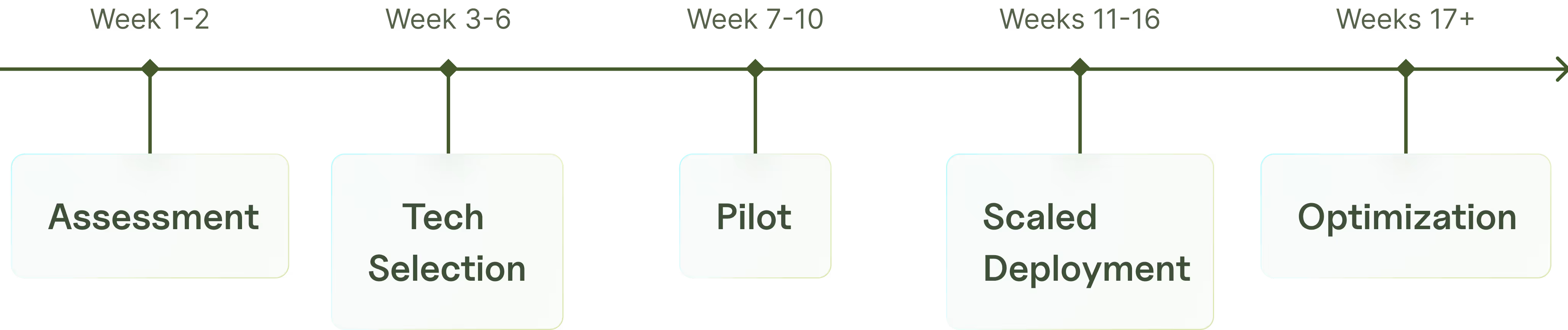

Phase 1: Assessment and goal setting (weeks 1-2)

Begin by mapping current claims workflows in granular detail. Document every step from initial call through final payment, noting handoffs, decision points, and bottlenecks. Track key metrics:

- Average time from FNOL to settlement

- Cost per claim processed

- Error rates in data entry and documentation

- Customer satisfaction scores

- Adjuster capacity and workload distribution

Identify high-volume, repetitive processes that consume disproportionate staff time. Simple auto claims, property damage reports, and routine medical claims typically offer the best automation opportunities. Set specific, measurable goals: reduce processing time by 40%, cut data entry errors by 70%, or increase adjuster capacity by 30 cases per month. Clear targets enable accurate ROI calculation and provide benchmarks for measuring progress.

Phase 2: Technology selection and integration planning (weeks 3-6)

Evaluate automation platforms based on several critical factors. Integration capability with your existing agency management system matters more than feature breadth - the most sophisticated platform creates minimal value if it can't share data ly with your AMS. Consider compliance features, particularly HIPAA requirements for health-related claims and state-specific regulatory standards for P&C processing.

Cloud-based solutions typically offer faster implementation and lower upfront costs compared to on-premise systems. Look for platforms that provide pre-built connectors for popular AMS platforms like Applied Epic, Vertafore AMS360, or HawkSoft. Comprehensive integration capabilities reduce implementation time from months to weeks while minimizing disruption to daily operations.

Phase 3: Pilot program (weeks 7-10)

Launch with a limited scope - perhaps automating FNOL intake for auto claims or document processing for property damage reports. Select a small team of adaptable staff members who will champion the technology and provide candid feedback. This contained pilot allows you to identify issues, refine workflows, and build internal expertise before broader rollout.

Monitor performance metrics daily during the pilot. Compare processing times, error rates, and customer satisfaction scores against baseline measurements from Phase 1. Track both quantitative metrics and qualitative feedback from staff and customers. Most agencies see measurable improvements within the first two weeks as teams adapt to new workflows and the AI models learn from initial interactions.

Phase 4: Scaled deployment (weeks 11-16)

Expand automation to additional claim types and team members based on pilot learnings. Provide comprehensive training that emphasizes how automation enhances rather than replaces human expertise. Position the technology as a tool that eliminates tedious work, allowing adjusters to focus on complex cases and relationship building.

Establish feedback loops where staff can report issues, suggest improvements, and share success stories. Create internal champions who model effective automation use and mentor colleagues struggling with the transition. Change management proves as critical as technology selection - the most powerful system fails if staff resist adoption or circumvent new processes.

Phase 5: Optimization and expansion (weeks 17+)

Review performance data monthly to identify optimization opportunities. Fine-tune ML models with accumulated data, adjust RPA workflows based on exception patterns, and expand voice AI capabilities to handle additional inquiry types. Continuously measure ROI and communicate wins to build organizational momentum for further automation investments.

Consider expanding to adjacent processes once claims automation matures. Policy renewals, customer service inquiries, and new business quoting follow similar automation principles and often share technology infrastructure. Strategic sequencing multiplies automation benefits by leveraging initial investments across multiple workflows.

Overcoming Common Implementation Challenges

Every agency encounters obstacles during automation implementation. Anticipating these challenges and preparing mitigation strategies separates successful deployments from abandoned initiatives that waste time and resources.

Data quality and system integration

Automation amplifies existing data problems. Inconsistent formatting, duplicate records, and incomplete information that human staff work around become blocking issues for automated systems. Address data hygiene before implementing automation - standardize naming conventions, cleanse duplicate records, and establish data entry standards that prevent future quality issues.

Legacy systems present integration challenges, particularly when multiple platforms handle different aspects of claims processing. Document all system touchpoints and data flows during the assessment phase. Some agencies require middleware or API development to connect disparate systems. Modern automation platforms offer pre-built connectors that reduce integration complexity, but custom connections may be necessary for older or highly customized AMS installations.

Staff resistance and skill gaps

Automation anxiety stems from legitimate concerns about job security and role changes. Address fears directly through transparent communication about how automation shifts rather than eliminates positions. Emphasize that routine task elimination creates capacity for higher-value work - complex claim analysis, customer relationship development, and strategic planning.

Invest in training that builds confidence with new tools. Some staff members adapt quickly to technology changes while others require additional support and practice time. Pair early adopters with skeptics to create peer mentoring relationships that accelerate learning and address concerns in relatable terms.

Regulatory compliance and security

Insurance operations involve sensitive personal and financial information subject to strict regulatory requirements. Automated systems must maintain audit trails, protect data privacy, and comply with state-specific insurance regulations. In 2025, insurers prioritize compliance with evolving data protection regulations including GDPR and CCPA, implementing secure storage and transmission protocols, and maintaining transparent audit trails with granular access controls.

Select vendors that demonstrate insurance industry expertise and regulatory knowledge. Request documentation of security certifications, compliance procedures, and data handling practices. Review service level agreements carefully to understand vendor responsibilities for data protection and regulatory compliance.

Balancing automation with human touch

Claims processing involves emotional situations - accidents, injuries, property loss - where empathy matters. Over-automation risks creating impersonal experiences that damage customer relationships. Design workflows that recognize when human intervention adds value versus when automation suffices.

Route complex, high-value, or emotionally charged claims to experienced adjusters while automating routine, straightforward cases. Use voice AI for initial intake and information gathering, then ly transfer to human adjusters when the situation warrants personal attention. Intelligent routing based on claim characteristics and customer sentiment ensures technology enhances rather than replaces the human relationships that define exceptional service.

Measuring Success: Key Performance Indicators and ROI

Quantifying automation impact requires tracking metrics across operational efficiency, customer experience, and financial performance. Establish baseline measurements before implementation and monitor changes monthly to demonstrate value and identify optimization opportunities.

Operational efficiency metrics

Processing time stands as the most visible efficiency indicator. Measure average days from FNOL to settlement for different claim types, tracking improvements as automation scales. Target 40-50% reduction in processing time for routine claims within the first six months. Monitor adjuster capacity by tracking cases handled per adjuster per month - automation typically increases capacity by 25-35% by eliminating data entry and routine inquiries.

Error rates provide a quality indicator. Track data entry mistakes, documentation omissions, and payment errors. Well-implemented automation reduces errors by 70-80% through consistent data capture and validation rules that catch mistakes before they cascade through workflows. Exception rates also merit tracking - monitor how frequently automated processes require human intervention to identify workflow improvements.

Customer experience indicators

Customer satisfaction scores often improve dramatically with automation. Survey policyholders after claim settlement to gauge satisfaction with communication speed, process transparency, and outcome fairness. Agencies implementing intelligent automation report satisfaction increases of 15-25 percentage points as customers appreciate faster responses and proactive updates.

First call resolution rates measure how often customers receive complete answers or service during initial contact. Voice AI systems that access full policy details and claim history enable representatives to resolve inquiries immediately rather than requiring callbacks or research time. Track Net Promoter Score (NPS) monthly - agencies consistently see NPS gains of 10-15 points following automation deployment as service speed and consistency improve.

Financial performance metrics

Cost per claim processed captures direct efficiency gains. Calculate total claims processing costs (staff time, technology, overhead) divided by claims volume. Most agencies see 20-30% cost reductions within the first year as automation handles routine work previously requiring multiple staff touches. Track return on investment by comparing implementation and ongoing costs against measurable savings from reduced processing time, lower error rates, and increased adjuster capacity.

Revenue impact proves harder to quantify but matters significantly. Faster claim settlement and superior customer experience improve retention rates and generate referrals. Track retention percentages for policyholders who have filed claims - agencies with automated claims processing typically see retention rates 5-8 percentage points higher than industry averages. Monitor organic growth from referrals by asking new customers how they heard about your agency.

Calculating comprehensive ROI

Build a complete financial model that captures both hard and soft benefits. Hard benefits include reduced staffing costs, eliminated overtime, and lower error correction expenses. Soft benefits encompass improved retention value, increased referral revenue, and competitive differentiation that supports premium pricing. Most agencies achieve positive ROI within 12 to 18 months, with benefits accelerating in years two and three as automation expands and staff expertise deepens.

Future Trends: What's Next for Claims Automation

Automation capabilities continue advancing rapidly. Understanding emerging trends helps agencies plan strategic investments and maintain competitive positioning as technology evolution accelerates.

Predictive analytics and proactive claims management

ML models increasingly predict claims before they occur. Weather data, property characteristics, and historical patterns enable insurers to identify high-risk situations and contact policyholders proactively with prevention recommendations. This shift from reactive to proactive claims management reduces frequency and severity while strengthening customer relationships through demonstrated concern.

Telematics data from connected vehicles provides real-time information about driving patterns, accident circumstances, and impact severity. Automated systems trigger FNOL workflows instantly when sensors detect a collision, dispatching emergency services if needed and initiating claim intake before the policyholder even calls. Similar IoT sensors in properties detect water leaks, fire conditions, and security breaches - enabling immediate response that minimizes damage.

Blockchain for claims verification

Blockchain technology creates immutable records of policy terms, claim submissions, and settlement payments. This transparency reduces disputes, accelerates verification processes, and prevents fraud through shared visibility among all parties. Smart contracts automate payment triggers when predefined conditions are met - hurricane winds exceed specified speeds, medical treatment reaches certain thresholds, or damage estimates fall below established limits.

Virtual and augmented reality for damage assessment

VR and AR technologies enable remote damage inspection with unprecedented detail. Policyholders use smartphone apps to capture 360-degree property views or vehicle damage imagery. AR overlays guide them to capture specific angles and details that adjusters need for accurate estimates. This capability eliminates scheduling delays for on-site inspections while maintaining assessment accuracy. Remote assessment capabilities proved critical during pandemic restrictions and remain valuable for improving speed and reducing adjuster travel time.

Hyper-personalization through AI

Advanced AI systems analyze individual policyholder communication preferences, claim history, and risk profiles to deliver personalized experiences. Some customers prefer text updates while others want phone calls. Some appreciate detailed explanations while others want concise summaries. AI-driven personalization adapts communication style, channel selection, and information depth to individual preferences - increasing satisfaction while reducing inquiries.

Conclusion: Taking the First Step Toward Transformation

Traditional claims processing buckling under modern pressures threatens agency profitability and customer retention. The $170 billion in premiums at risk by 2027 represents lost opportunities for agencies that fail to modernize workflows and meet evolving customer expectations. Yet the transformation path remains clear: automation reduces processing times by 50%, cuts costs by 20-30%, and increases customer satisfaction by more than 60% - creating measurable competitive advantages that compound over time.

We've worked with hundreds of agencies navigating this transformation at Sonant AI. The pattern proves consistent: agencies that start with focused pilot programs, prioritize integration with existing systems, and invest in staff training see positive ROI within 12 to 18 months. More importantly, they reclaim valuable production time that shifts from routine data entry to relationship building and business development. Every incoming claim call becomes an opportunity to strengthen client bonds rather than a task that pulls adjusters away from strategic work.

The technology offers powerful capabilities - from voice AI that handles FNOL with natural conversation to ML models that detect fraud and predict outcomes. Success requires matching these capabilities to specific agency needs and workflows. Start by assessing current processes, identifying high-impact automation opportunities, and selecting platforms that integrate ly with your AMS. Launch with a contained pilot that builds internal expertise and demonstrates value before scaling across the organization.

The competitive stakes continue rising as early adopters pull ahead and customer expectations shift toward immediate, 24/7 service. Climate change drives claim volumes higher while talent shortages constrain agency capacity. Automation addresses both pressures simultaneously - increasing throughput while reducing dependence on scarce human resources. The question shifts from whether to automate to how quickly you can implement systems that protect market position.

The agencies thriving in 2026 recognize that every phone call represents a revenue opportunity rather than a routine interruption. They've built technology infrastructure that captures these opportunities consistently, delivering superior experiences that drive retention and referrals. The competitive edge comes from strategic automation that amplifies human expertise rather than replacing it - freeing talented adjusters to focus on complex cases and relationship development that technology cannot replicate.

When the phone rings, we're already there.

The AI Receptionist for Insurance

FOLLOW SONANT ON

.svg)

.svg)