.svg)

.avif)

How to get more leads as an insurance agency is the wrong first question at most agencies, the right one is "how many of the leads we already get are we converting?" A typical P&C (property and casualty) agency misses 12–18% of inbound calls and loses most after-hours quote shoppers entirely, which means the cheapest lead source is the leak. Once capture is fixed, the playbook is real: referral systems that actually run, local search presence, retention-driven cross-sell, and paid channels with the phone layer to convert them. This piece is the full sequence, ordered by cost per acquired policy.

Key Takeaways

- The cheapest "new" leads are the inbound calls currently leaking to voicemail and after-hours

- Referrals remain the highest-converting source, but only when the ask is systematic, not occasional

- Local search (Google Business Profile + reviews) is the highest-ROI organic channel for agencies

- Paid leads work only when speed-to-contact is under 5 minutes, which is a phone-layer problem

- Every lead source funnels through the same chokepoint: whether the call gets answered

Step 0: Fix capture before buying anything

Run the math before spending: at 250 inbound calls a month and a 15% miss rate, the agency loses roughly 18 paid-for opportunities monthly; recurring. Fixing the capture layer (first-ring pickup 24/7, English and Spanish, after-hours coverage) converts existing marketing spend better and raises the ROI of every channel added afterward. The J.D. Power shopping data is blunt about why: quote shoppers comparison-shop in real time, and the agency that answers first usually wins.

Want your capture baseline measured first? → Talk to Sonant

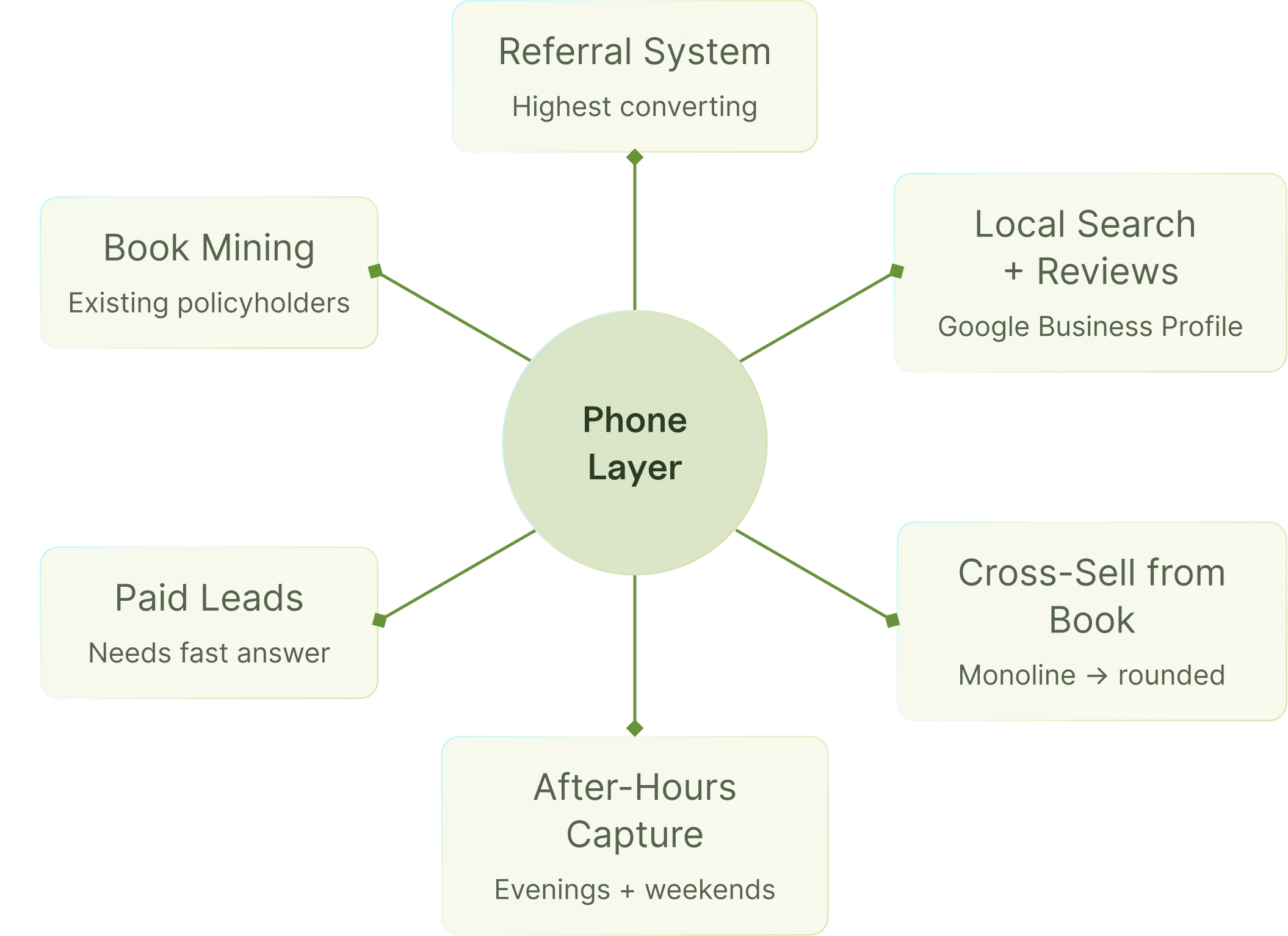

Step 1: Systematize referrals, the highest-converting source

Referred leads close at multiples of cold-lead rates and cost almost nothing. The difference between agencies that get them and agencies that wish they did is a system:

- Ask at the moments of delivered value: after a smooth claim, a same-day certificate, a renewal save, not randomly

- Make the ask specific: "who do you know who just bought a house?" outperforms "send anyone our way"

- Track and thank: every referral logged in the AMS (agency management system), every referrer thanked within 48 hours

- Mine the book: commercial clients know other business owners; new homeowners know other new homeowners

The channels in this playbook, ordered the way the article argues them, by cost per acquired policy:

Step 2: Own your local search presence

When someone searches "insurance agency near me" or "[your town] auto insurance," the map pack decides who gets the call. The checklist: a complete Google Business Profile (hours, services, photos), a steady review cadence (ask after every positive interaction; agencies with 50+ recent reviews dominate local results), and consistent name-address-phone across directories. This channel costs effort, not budget, and compounds for years.

Step 3: Cross-sell the book you already have

Monoline customers are pre-qualified leads sitting in your AMS: the auto-only household that owns a home, the homeowner without an umbrella, the business owner with no cyber coverage. A freed-up service team running account-rounding blocks converts these at warm-call rates, and every rounded account also retains better, which compounds the math.

Step 4: Add paid channels, with the conversion layer ready

Paid search, social, and purchased internet leads all work, at the right cost discipline and only with instant response. Speed-to-contact is the entire game on paid: conversion drops roughly 4× between a 5-minute response and a one-hour response. Before funding any paid channel, confirm the phone layer answers instantly across all hours, including the 8 PM clicks your business-hours team will never see. The ACT benchmarks on response timing make this the make-or-break variable for paid ROI.

The Sonant Consumer AI Readiness Report reinforces it from the shopper side: first responder usually wins, and shoppers do not distinguish between channels, they distinguish between answered and unanswered.

Step 5: Publish content that answers buyer questions

Local-intent content ("[state] auto insurance requirements," "what does an umbrella policy cover") builds the organic pipeline over quarters, not weeks. It is the slowest channel here and the most durable, every piece keeps producing. Pair it with the local-SEO work from Step 2; they feed each other.

The chokepoint every source shares

Referral, map-pack click, cross-sell trigger, paid lead, every source ends at the same place: a phone call to your agency. The lead playbook's hidden multiplier is the layer that answers that call at first ring, qualifies the shopper, books the producer appointment, and writes the AMS note, at 2 PM and at 9 PM, in English and Spanish. Improving the phone layer raises every channel's yield simultaneously; no other single investment touches all of them at once.

How Sonant multiplies every lead channel

Sonant is the conversion layer under the whole stack: first-ring pickup 24/7 in English and Spanish, quote-shopper qualification, producer appointments booked on the call, and AMS write-back within 60 seconds to EZLynx, Applied Epic, HawkSoft, AMS360, QQCatalyst, Momentum, AgencyZoom, and Zywave, with cross-sell triggers flagged from service calls feeding Step 3 automatically. Output is a capture rate above 97% on every channel's output, which is the difference between buying leads and buying growth.

The practical takeaway for the agency that wants more leads

Get more leads as an insurance agency in cost order: capture the leak first, systematize referrals, own local search, round the monoline book, then add paid with the response layer ready. Run the channels through one measured phone layer and re-check cost per acquired policy quarterly. Most agencies discover the first two steps alone fill the producer calendars they thought required a bigger marketing budget.

Ready to convert every channel you already have? Book a Sonant demo →

Related reading

Founding Sr. AE & Team Lead

FOLLOW SONANT ON

.svg)

.svg)