.svg)

AI is changing the insurance industry in 2026 across four operational layers: inbound call handling, renewal sequencing, FNOL (first notice of loss) intake, and submission quality at the carrier appetite step. For a retail P&C (property and casualty) agency, the practical question is not whether AI will reshape the business. It is which two or three workflows to deploy first, which AMS (agency management system) integrations matter, and what to ask in a vendor demo. This guide answers each of those questions for an agency operations leader. Most agencies miss calls during renewals, claims, or busy service hours - Sonant helps make sure those calls are still answered.

Key Takeaways

- AI is changing the insurance industry primarily at the call handling layer, not at the underwriting layer

- The four mature 2026 use cases at retail agencies: inbound voice, renewal outbound, FNOL intake, post-bind sequences

- AMS write-back fidelity is the single feature that decides ROI on any deployment

- A 30-day pilot on overflow traffic is the right way to evaluate vendors without disrupting the call flow

- Most agencies cut routine workload 40–60% within 6 months on the right platform

Where AI is actually showing up at retail insurance agencies

AI is showing up at the front door of the agency - the phone line, the after-hours overflow, and the renewal outbound queue. These are the workflows where call volume, language coverage, and AMS write-back coincide. CSRs (customer service reps) still own the complex commercial servicing. AI handles the routine 40–60% that used to spill to voicemail.

Concrete examples from the day-to-day:

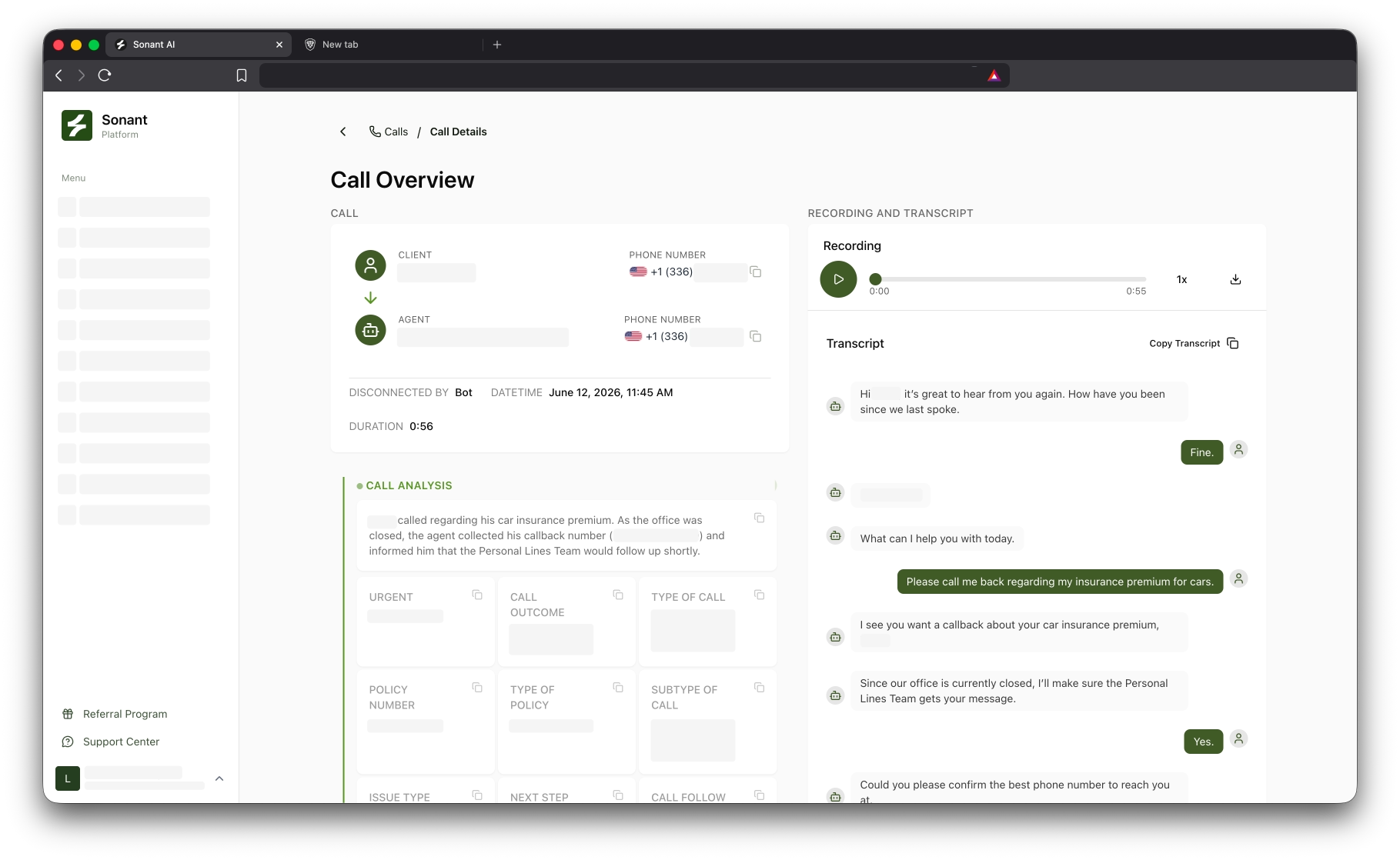

- A homeowners shopper calls at 7:42 pm. The AI receptionist answers, captures intent, runs the address through carrier appetite, and books a 10:30 am producer call for tomorrow.

- A renewal call at 60 days out goes outbound. The AI confirms the dec page, captures a vehicle change, and routes the change to the producer queue.

- An FNOL call comes in on a Saturday. The AI captures the loss details, fills the ACORD (industry data standard) form, and routes to the carrier portal.

These are not future workflows. They are running in 2026 at agencies between 5 and 500 employees. The Sonant Consumer AI Readiness Report confirms that policyholders increasingly expect AI-handled service interactions across exactly these workflows.

See how Sonant fits into your day-to-day → Talk to Sonant

How AI is changing insurance underwriting (and why it matters less to agencies)

AI is changing insurance underwriting at the carrier level. Carriers are running submissions through automated appetite checks, declining sub-segments faster, and pricing tighter on the risks they bind. For agencies, the practical impact is asymmetric: clean submissions get faster bind, sloppy submissions get faster decline.

Most retail agencies do not need to deploy underwriting AI themselves. The right move is to use AI on the submission quality side - pre-check submissions against carrier-specific data requirements before sending. The reduction in decline rates is measurable within 90 days.

What changes on the customer experience side

The customer experience layer is where AI changes the most observable agency metric: first-ring pickup rate. The industry baseline sits at 70–82% during business hours and drops below 50% after 6 pm and on weekends. AI moves first-ring pickup above 95% across 24/7, English and Spanish, without adding headcount.

The downstream effects compound:

- Voicemail backlog drops to near-zero

- Response time on routine service requests falls from hours to seconds

- Spanish-speaking caller abandonment drops from 15–35% to under 5%

- Follow-up completion improves because every interaction writes to the AMS

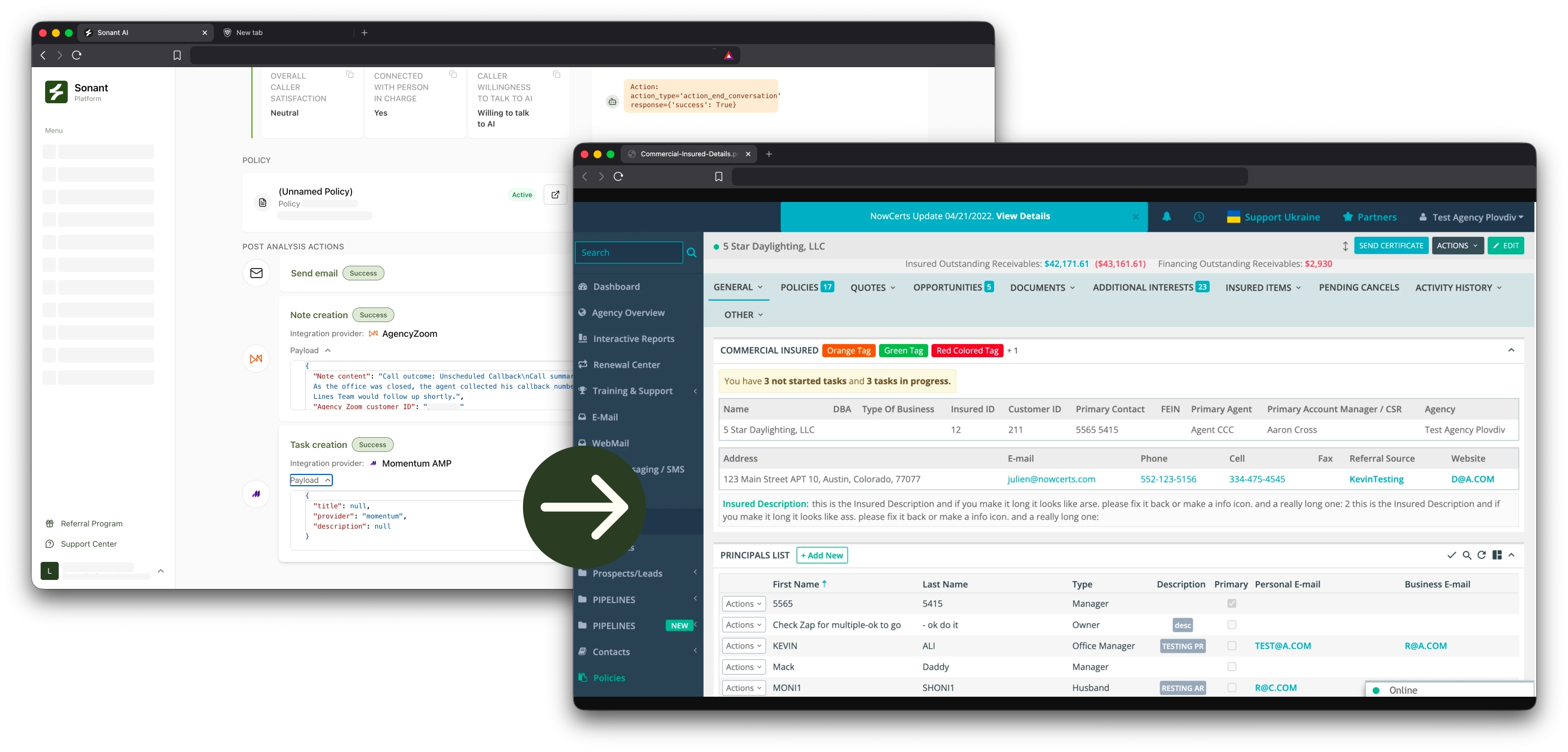

Which AMS integrations matter

The AMS is the durable system. AI vendors come and go. The integration is the make-or-break factor. For agencies running on EZLynx, Applied Epic, HawkSoft, AMS360, QQCatalyst, Momentum, AgencyZoom, or Zywave, native write-back is non-negotiable. Middleware (Zapier, custom API work) breaks the first time the AMS releases an update.

A vendor that publishes an integrations page listing your AMS by name is the starting point. A vendor that demos AMS write-back live, on your platform, in the sales call is the right answer.

How to evaluate AI vendors in 2026

The five-question vendor demo framework that operations leaders are running:

- Show live AMS write-back on the platform we use - demo, not a slide

- Walk through a non-renewal call from caller intent to AMS note

- Demonstrate Spanish handling at the first ring

- Quote per-call cost at 600 calls/day, 1,200 calls/day, and 2,000 calls/day

- Share one case study from an agency in our size range

If a vendor cannot answer all five with specifics, the vendor is not the right fit.

How Sonant fits into the AI shift at retail agencies

Sonant is an AI receptionist built specifically for retail P&C insurance agencies. The platform answers inbound calls, captures caller intent, books appointments, writes the AMS note within 60 seconds of the call ending, and escalates urgent requests to licensed staff. Native integrations cover EZLynx, Applied Epic, HawkSoft, AMS360, QQCatalyst, Momentum, AgencyZoom, and Zywave. Deployment runs under 30 days with white-glove implementation. The workflow Sonant absorbs is the routine 40–60% of inbound - leaving CSRs to handle complex commercial servicing where human judgment matters.

The practical takeaway for agency operations leaders in 2026

AI is changing the insurance industry at the call handling layer first, the renewal sequence second, and the FNOL intake layer third. For a retail agency, the sequencing is straightforward: deploy AI on inbound overflow in months 1–3, expand to after-hours and weekends in months 4–6, add renewal outbound and FNOL intake in months 7–12. Pick a vendor with native AMS write-back. Pilot on overflow before touching primary flow. Most agencies running this sequence see payback within 6–9 months.

Ready to see how AI fits your agency’s day-to-day? Book a Sonant demo →

Related reading

Co-founder & CEO

FOLLOW SONANT ON

.svg)

.svg)