.svg)

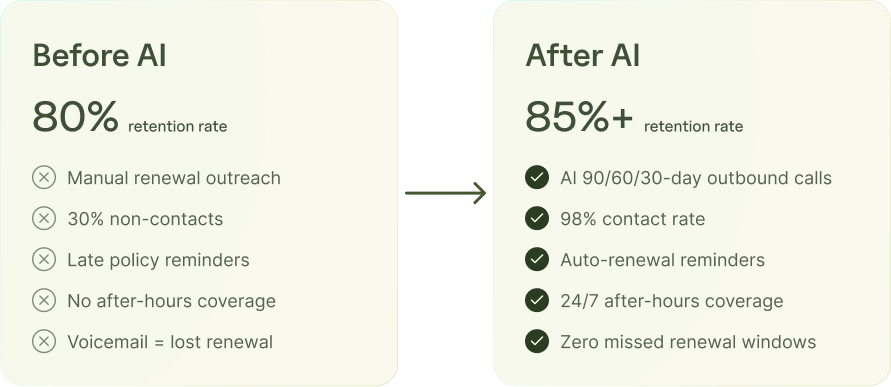

Customer retention at an insurance agency moves with three operational levers: renewal sequence consistency, follow-up completion on service requests, and response time at the call layer. Industry retention sits at 84–89% at top-quartile P&C (property and casualty) agencies; median is closer to 80%. A 5-point retention lift on a $25M book is worth $1.25M annual recurring revenue. This piece is the 90-day plan to move retention - the levers, the metrics, and the order to run them. A missed call is not just a missed conversation; it can be a missed renewal, claim update, or service request, which is where most retention leaks start.

Key Takeaways

- Retention moves with three levers: renewal sequence consistency, follow-up completion, response time

- A 5-point retention lift on $25M book = $1.25M ARR

- The 90/60/30-day automated renewal sequence is the largest single retention lever

- AMS (agency management system) write-back at the call layer is the prerequisite for measurable retention work

- Most retention shifts show in 6–12 months, not 30 days

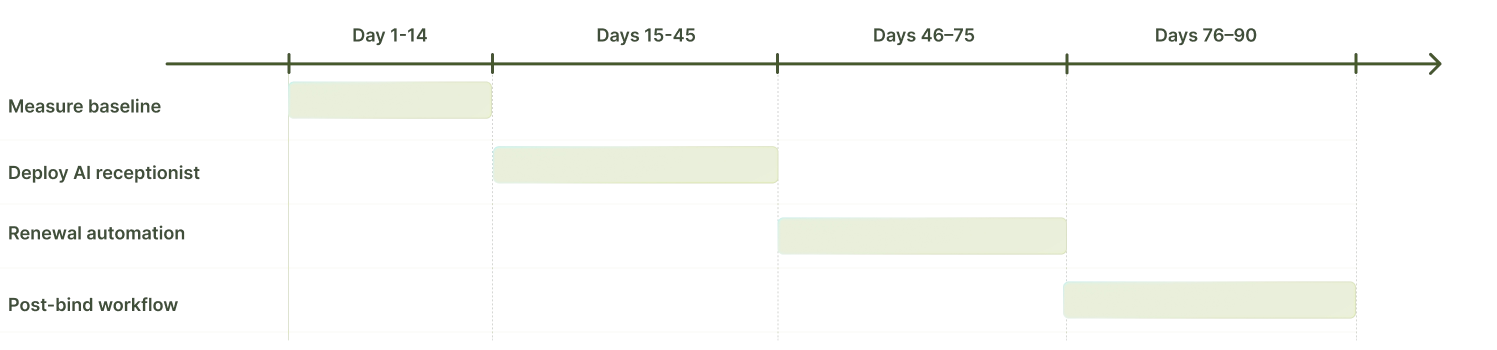

Step 1: Measure the retention baseline

Most agencies do not know their per-segment retention. They should. The metrics to capture for a 90-day baseline:

- Overall retention rate (book-wide, last 4 quarters)

- Retention by line of business (personal auto, home, commercial)

- Retention by tenure (year 1, year 2+, year 5+)

- Voluntary vs involuntary churn split

- Top 50 churn reasons (from exit interviews or carrier feedback)

Your AMS (agency management system) should report most of this. If it does not, fix the reporting before fixing retention.

Step 2: Automate the 90/60/30-day renewal sequence

The largest single retention lever. Most agencies run renewal outreach manually – producers calling their book in spare time. The execution is inconsistent. Automated renewal sequences run outbound calls in the right window, capture confirmations or changes, and route complex cases to producers. Lift: retention +2–4 points within 6 months.

Want help running the renewal sequence automatically? → Talk to Sonant

Step 3: Fix follow-up completion on service requests

Service requests that go untouched are a quiet retention killer. The fix is AMS write-back at the call layer + workflow triggers on the AMS note. Every interaction logged, time-stamped, attached to the right account. Every open task surfaced. Lift: retention +1–2 points.

The Sonant Consumer AI Readiness Report provides additional benchmarks on how policyholders rate AI-handled service interactions across the retention-critical dimensions.

Step 4: Cut response time on inbound from hours to seconds

Industry baseline first-ring pickup runs 70–82% business hours, below 50% after 6 pm. AI receptionist moves first-ring pickup above 95% across 24/7. Lift: retention +1–2 points + NPS (net promoter score) +5–10.

Step 5: Run the post-bind welcome call within 48 hours

Personal lines automation is mature for the welcome call workflow. Confirms coverage, captures cross-sell triggers, sends the carrier docs. Lift: retention +2–3 points on year-1 cohort.

Step 6: Audit the top 50 churn calls quarterly

The transcripts tell you what is breaking. Coverage misunderstandings, billing surprises, claim experiences, agent-of-record changes. Each one is a process gap to close. Lift: compounding, variable.

Step 7: Send NPS surveys post-call automatically

Closes the feedback loop before issues compound. Trigger when AMS note posts. Lift: NPS +2–3, which leads retention.

Step 8: Train CSRs (customer service reps) on tier-2 complex servicing

AI absorbs tier-1 routine. CSRs focus on the complex commercial servicing and high-value account work where the relationship matters. Lift: retention +1–2 points (CSR attention quality up).

The 90-day retention sequence

By day 90, NPS should be measurably up. Retention follows in months 4–12.

How Sonant runs the retention workflow

Sonant absorbs the renewal outbound sequence, the post-bind welcome workflow, the first-ring pickup on inbound, and the AMS write-back at the call layer. Native integrations cover EZLynx, Applied Epic, HawkSoft, AMS360, QQCatalyst, Momentum, AgencyZoom, and Zywave. The workflow: renewal due date hits → Sonant runs the 90/60/30 outbound → captures confirmation or change → routes complex cases to producer → writes the AMS note. Output is the renewal status confirmed in the AMS plus the calendared producer handoff where needed.

The 90-day retention plan most agencies can run

Measure the baseline by segment, deploy AI receptionist for first-ring pickup and AMS write-back, automate the renewal sequence, layer the post-bind welcome workflow. NPS lifts in 30 days, retention lifts in 4–12 months. A 5-point retention move on a $25M book = $1.25M ARR. The plan above is what agencies running it actually see.

Ready to operationalize retention at your agency? Book a Sonant™ demo →

Related reading

Founding Sr. AE & Team Lead

FOLLOW SONANT ON

.svg)

.svg)