.svg)

.avif)

Insurance business process outsourcing (BPO) at a P&C (property and casualty) agency in 2026 does not look like it did in 2022. The Philippines back-office model still works for high-touch commercial servicing. Everything else, including inbound calls, renewal outreach, COI (certificate of insurance) generation, FNOL (first notice of loss) intake, and post-bind sequences, is being absorbed by AI. This guide is the playbook for operations leaders making the buy decision in 2026: where BPO still wins, where AI is replacing it, and how to sequence the transition without breaking the team.

Key Takeaways

- AI is replacing 60–70% of historical BPO scope at retail P&C agencies

- The complex 30–40% (commercial servicing, certificate management at scale, multi-language beyond Spanish) stays with humans

- The hybrid model (AI + reduced BPO) is the 2026 default

- AMS (agency management system) write-back is the field that flips most BPO decisions toward AI

- The 9-month transition prevents service gaps

The state of insurance BPO in 2026

The traditional Philippines BPO model, where offshore CSRs (customer service reps) handle data entry, document processing, and overnight servicing, grew through 2018–2022 as a way to expand capacity without paying US wages. The model works. But the economics have shifted twice in 24 months:

Shift 1: AI took the lowest-complexity work. Routine inbound calls, COI generation, billing inquiries, claim status updates, renewal outbound. All automatable at $0.40–$1.20 per call versus $1.50–$3.50 per call for offshore live.

Shift 2: AMS write-back stopped being optional. Offshore CSRs without native AMS access transcribe notes manually, often with delays. AI-native automation writes directly to the AMS in real time. For agencies running governance reviews or selling to PE acquirers, the audit trail matters.

The net effect: AI is replacing the routine 60–70% of BPO scope. The remaining 30–40% (complex commercial servicing, mid-term endorsements, certificate management for high-touch accounts) stays with humans.

.avif)

The Sonant Consumer AI Readiness Report provides consumer-side benchmarks on how policyholders rate the AI-handled portion of the hybrid model.

Where offshore BPO still wins

Complex commercial servicing. Large commercial accounts with bespoke endorsements, mid-term changes, and carrier-specific quirks need experienced staff. The BPO model is still cost-effective compared to in-house US hires for this work.

Certificate management at scale. Construction, trucking, and contractor accounts that issue 50+ COIs per month per account. The volume justifies dedicated offshore staff.

Document-heavy underwriting support. Commercial submissions with policy docs, loss runs, financial statements, and ACORD (industry data standard) forms. The document processing portion is moving to AI; the underwriting-adjacent judgment work still benefits from human attention.

Multi-language servicing beyond Spanish. Vietnamese, Mandarin, Korean, Arabic. The major AI platforms handle English and Spanish well; depth in other languages still favors traditional BPO.

Want help sequencing the BPO-to-AI transition? → Talk to Sonant

Where AI is replacing BPO

Inbound voice. The biggest category by call volume. AI handles 24/7 first-ring pickup, qualifies callers against the AMS, processes routine servicing, routes complex cases. Cost per call is 25–40% of offshore live.

Renewal outbound. The 90/60/30-day sequence is fully automatable. AI runs the calls, captures responses, processes simple changes, routes complex cases to producers.

COI and certificate generation. Standard certificates generated on the call by AI. High-volume construction accounts may still need human review; long-tail one-off COIs run cleanly through automation.

FNOL intake. Loss detail capture, ACORD form fill, carrier portal routing. Downstream claim handling stays with carriers and adjusters.

Post-bind sequences. Welcome calls, NPS (net promoter score) surveys, review requests, cross-sell triggers. All automatable at scale.

What 600 inbound calls a day costs across pure BPO, pure AI, and hybrid

The hybrid model is the 2026 default for retail P&C agencies.

What compliance posture you need from a BPO vs an AI vendor

Traditional BPO compliance varies. Some Philippines vendors hold SOC 2 Type 2; many do not. Data residency depends on where the BPO’s servers live. For agencies handling commercial accounts with sensitive data (especially financial services, healthcare-adjacent, or government contractors), the compliance gap matters.

Insurance-native AI platforms (Sonant, Liberate, Cara) publish SOC 2 Type 2 and GDPR documentation. Some offer HIPAA BAAs (business associate agreements). For PE-backed agencies, compliance posture is a procurement requirement, not a nice-to-have.

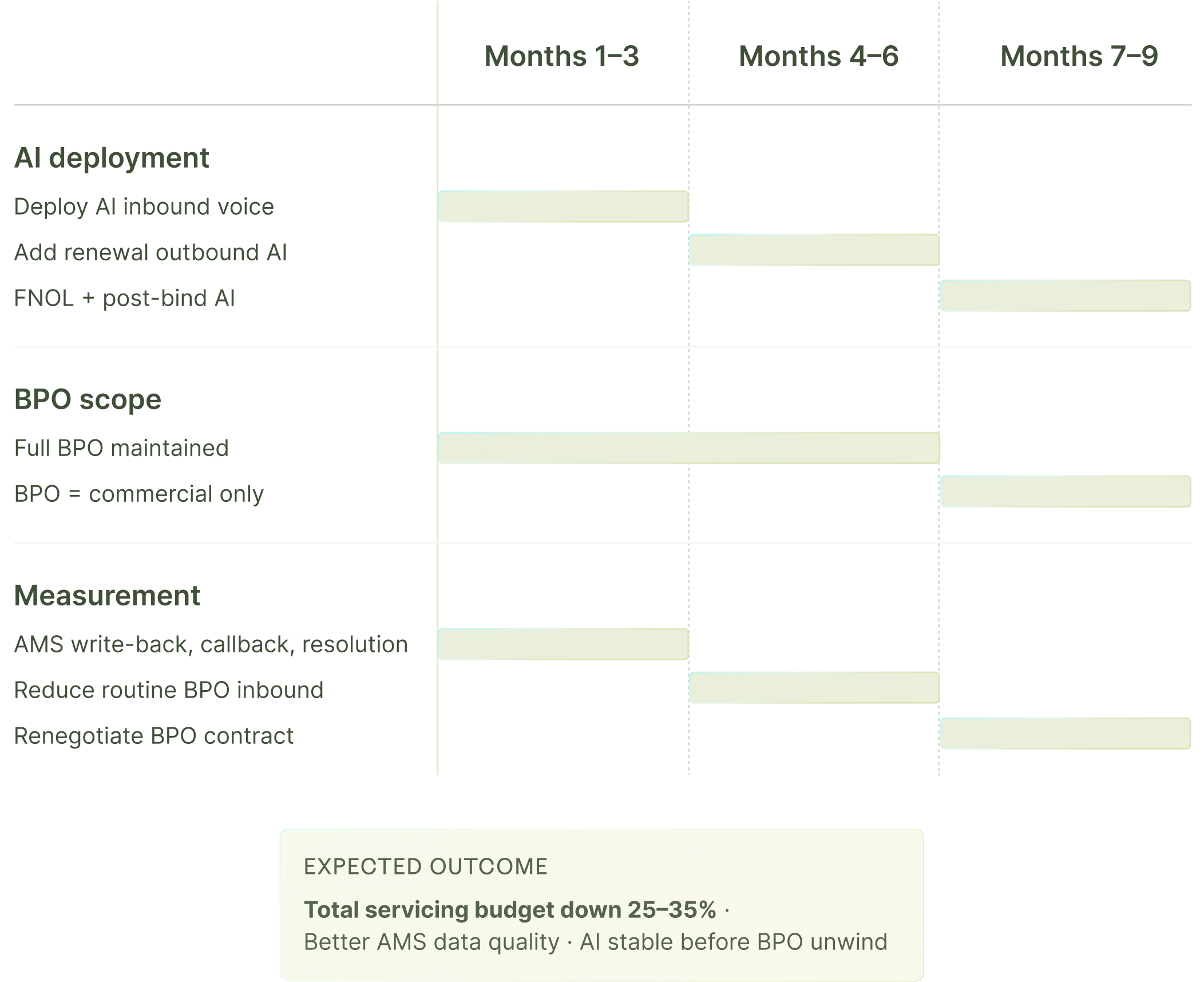

Transition playbook for an agency on a 9-month timeline

Months 1–3. Deploy AI for inbound voice (quote intake + servicing). Do not cut BPO yet. Measure AMS write-back accuracy, callback conversion, Spanish-speaker capture, average call resolution.

Months 4–6. Layer in AI for renewal outbound. Begin reducing BPO scope on routine inbound - keep offshore on commercial servicing only.

Months 7–9. Move FNOL intake and post-bind sequences to AI. Renegotiate BPO contract to focus on the 30–40% commercial-heavy work that stays. Expect total servicing budget down 25–35% with better data quality.

The agencies that try to cut BPO before AI is stable usually fail. The order matters: prove AI, then unwind BPO.

Which BPO, AI, and hybrid vendors actually compete in 2026

Traditional BPO providers. ResourcePro, Patra, Cover Desk, Agency VA, My Outdesk, Virtual Intelligence. Strong on commercial servicing depth, weak on automation. Best as part of a hybrid stack.

AI-first insurance platforms. Sonant, Liberate (carrier-focused), Cara by Capacity. Built for the routine 60–70% workload. Native AMS write-back.

Hybrid offerings. Some BPO providers are layering AI on top. Maturity varies. Picking the best AI vendor + best BPO vendor separately usually beats a single hybrid.

When to keep BPO, when to replace it

Keep BPO for: complex commercial servicing, certificate management at scale, multi-language beyond Spanish, document-heavy underwriting support.

Replace BPO with AI for: inbound voice, renewal outbound, routine COIs, FNOL intake, post-bind sequences, lapsed-policy recovery.

How Sonant fits the hybrid BPO model

Sonant handles the routine inbound voice and outbound renewal workflows that were previously the bulk of BPO scope. Native integrations to EZLynx, Applied Epic, HawkSoft, AMS360, QQCatalyst, Momentum, AgencyZoom, and Zywave. The workflow: call comes in or renewal triggers → Sonant runs the step → captures details → writes the AMS note within 60 seconds → routes complex cases to the BPO commercial team. Output is the AMS-attached note plus the routed case.

ROI: typical 12-month numbers for mid-market agencies

An agency with $1.5M annual servicing budget transitioning to a hybrid AI + reduced BPO model typically sees:

- Direct cost savings: $400K–$700K annually

- Improved AMS data quality (measurable through audit trails)

- Producer time recovered for new business: 200–300 hours per producer per year

- New-business premium uplift on book

- NPS up 5–10 points from faster first-ring pickup

Payback on the AI investment is 4–7 months. The full transition pays for itself in year one.

Where BPO still wins in 2026 (and where it doesn’t)

Insurance BPO in 2026 is not disappearing - it is getting smaller and more specialized. The routine 60–70% of historical BPO scope is moving to AI. The complex 30–40% stays with humans, often still offshore. The right move for a P&C agency is the hybrid: pick the best AI platform for the routine, keep BPO for the complex, renegotiate scope on a 9-month timeline. Expected outcome: 25–35% lower total servicing cost with better data quality.

Related reading

Founding Account Executive

FOLLOW SONANT ON

.svg)

.svg)